We have talked about securities, stocks, mergers and acquisitions, but how do you calculate how much these investments are worth?

Financial value can be calculated in different ways; however, today we will be focusing on the most common one, the Discounting Cash Flows models (DCF).

Discounting cash flows is a fundamental concept in finance, used to determine the present value (PV) of future cash flows. The idea behind DCF is that money received in the future is worth less than the same amount of money received today. Therefore, if you inherit $100,000 from your rich uncle, DCF suggests that the 100k now is less than the initial 100k. This concept holds up because 100k today could be invested into multiple securities and liquidated further on in the future. Not only that, but money today is not worth the same as money in the future due to inflation and a subsequent decrease in purchasing power. This suggests that you can buy less things with the same amount of money, or alternatively, the same things with more money.

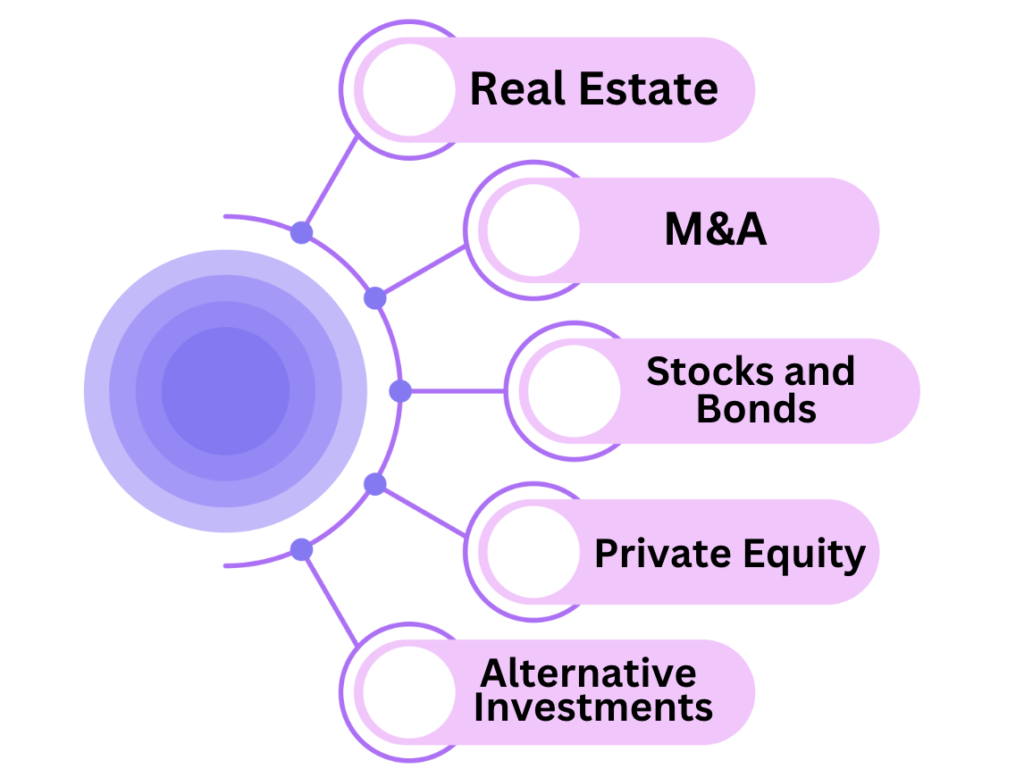

As seen below, DCF can be used to calculate the value of a variety of investments based on its cash flows. Nonetheless, DCF values are heavily subjective and some values may be inaccurate, so use this only as an estimate and not as a fail-proof value. As seen on the right, it can be used to calculate value from real estate to M&A and to stocks and bonds, which make it must more versatile than other valuation methods.

Now that we know what DCF is, let us put it to work and understand how to value an investment and see how we can go about this.

Step 1: Calculate Free Cash Flows

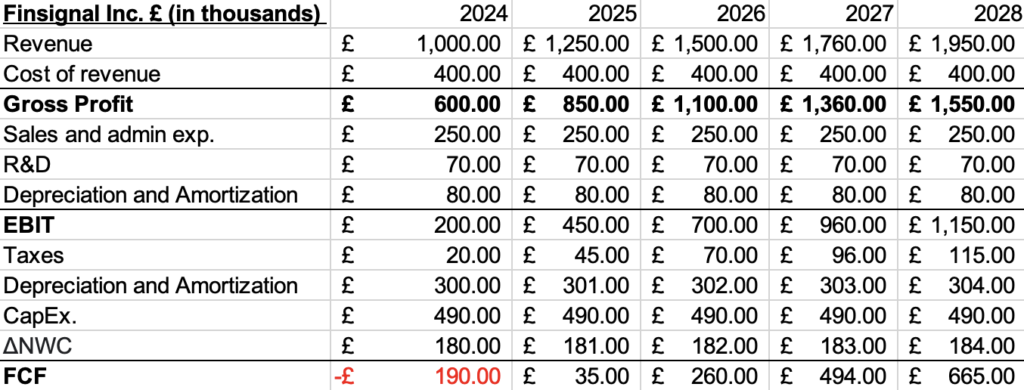

Our first step is to calculate free cash flows to the firm (equity and bondholders) by going through the income statement and getting EBIT (Earnings before interest and tax).

After calculating EBIT (below), we can work towards our FCF figure. We now need to get an aggregate figure that resembles our FCF. We add/subtract different variables to get to our final FCF figure.

Note: We subtract CapEx. (Capital Expenditure) because it is the required amount to run the business and keep it operational.

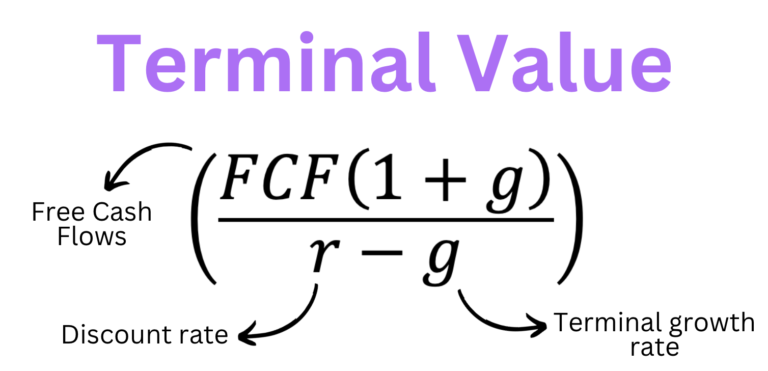

Step 2: Forecast the firm’s terminal growth rate

Just like most things in life, the firm’s value cannot grow infinitely, so we must calculate a terminal growth rate. Cash flows are usually forecasted for the next 5-10 years. After finding the cash flows for these desired time period, we need to assume that the firm is going to (more or less) have a stable growth rate thereafter. For this example, we will be using a growth rate of 4% But for now, we need to calculate the terminal value of the firm.

That is great and all but, what is our discount rate? Unfortunately, this is an unknown variable that we must calculate.

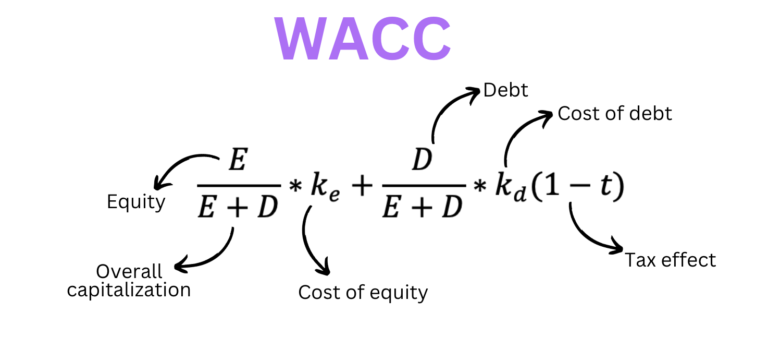

Step 3: Calculate the Weighted Average Cost of Capital (WACC)

This number is the rate of return required by the company’s bond and shareholders. We can use this as our discount rate because it is the minimum requirement for its investors; the riskier the investment, the higher the WACC. This model below has been simplified and excludes preferred stock, however it would include a third “part” if it were to be added on. The cost of equity and the cost of debt both have returns that need to be met; equity’s return is the shareholders’ demand for their investment and bondholders is the interest on the money borrowed.

As you can see, the debt part of the equation is slightly different to the equity part – this is because debt is tax deductible. This is why some companies adopt debt into their capital structure. This reduces the company’s taxable income, which is why debt is so attractive. Inversely, for equity, there is no obligation to repay the money. The cost of equity can also be calculated through CAPM, also known as the Capital Asset Pricing Model. This calculates the return you should ask as an investor for the money you put into the business. However, that is a story for another day. For example purposes, let us assume our discount rate is 8%.

Step 4: Plug-in our variable and obtain our share value

Ah, yes. Finally. Although, note that this is not a quick final step and it definitely sounds easier than it sounds. This final value will get us the firm’s Enterprise Value, or EV for short. For instance, let us assume that Finsignal Inc. is valued at £90,000,000. That is great and all, but we want to know what our share is worth as shareholders.

We now need to adjust the EV to obtain the company’s share value. To get to our final value, we need to subtract the market value (MV) of the debt we incurred and the MV of any preferred stock (if the company has any). We subtract the £30,000,000 worth of debt and get £60,000,000 of fair value. Now, we need to divide this figure by the company’s 10,000,000 outstanding shares (publicly available) and get £6 asa rough estimate of the value of the company’s share. Interestingly enough, the DCF formula allows us to see how different variables affect the overall value, which is why analysts tend to run a sensitivity analysis with new possible investments.

Essentially, no. If we have the possibility to buy a share of Finsignal Inc. for £9 and we calculated a share price of £6, then the almost-obvious answer would be to pass on the offer because the investment seems to be overvalued. Not only does the DCF show us the cash flows that an investment will generate, it also gives us a way to calculate whether a specific security or investment should be purchased.